The additions is: we adjust fees to attract liquidity providers and revenue for 1hive.

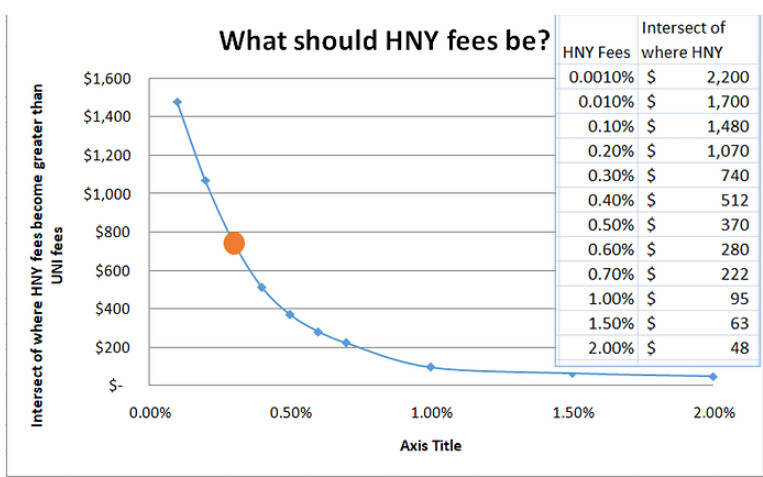

I believe or fee structure is in desperate need of a change, others have brought this up before. Interestingly, I replied stating our current 0.3% fee structure makes us completive up to $740 RTT. This is true but we are leaving a tremendous amount of profit for 1hive and liquidity providers on the table. Depending on mainnet fees we can easily support 5% fees up-to $100 swaps. But we don’t have to go that aggressive.

The 0.3% fee structure may work for UNI but it doesn’t work for us. Even when we saw the highest weekly volume, $8M was only a measly $575 a day for the 1hive and $2,850 for ALL the liquidity providers. That is no incentive at all.

Interestingly in that same forum post I stated the following:

Based on a previous analysis I think our target trader needs to be either:

Less than $650x2 = $1,300 RTT

or Less than $1,300x2 = $2,600 RTT

Unfortunately, under our currently liquidity levels we actually need to drop our fees to 0.1% to pick up our smallest ideal audience.

There are two key points here:

We need lower fees to target the traders in the above two ranges

and secondly, there was a flaw when I stated that we should lower LP fees while liquidity levels are low. (this flaw being obvious upon re-reading. LP fees attract liquidity, lowering fees would hurt levels even more)

The proposal

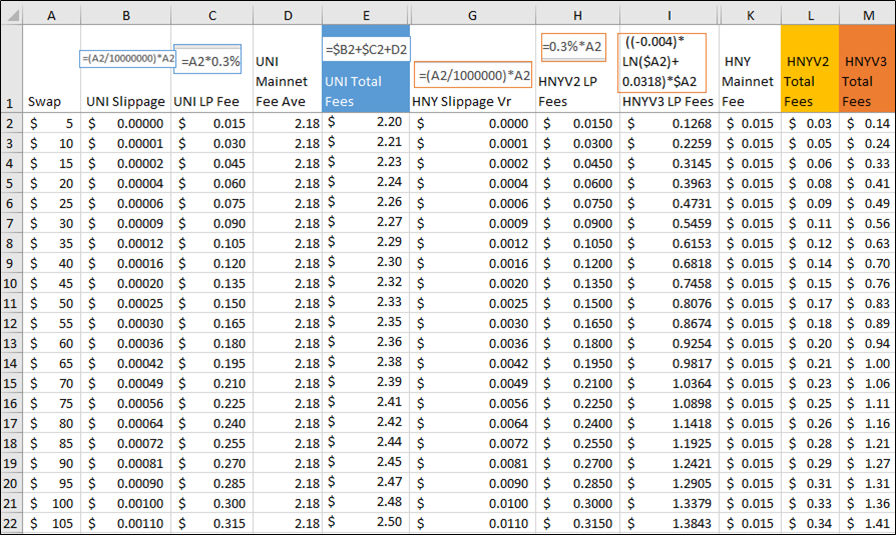

We raise LP fees for swaps less than $1,500. We can raise them just enough while staying competitive against the average ETH mainnet fees of $2. Then lower LP fees for swaps greater than $1,500. This proposal would look like the following for swaps up to $1,500:

y = -0.004ln(x)+0.0318 (or about 1.3%) from $0 to $1,500 swaps

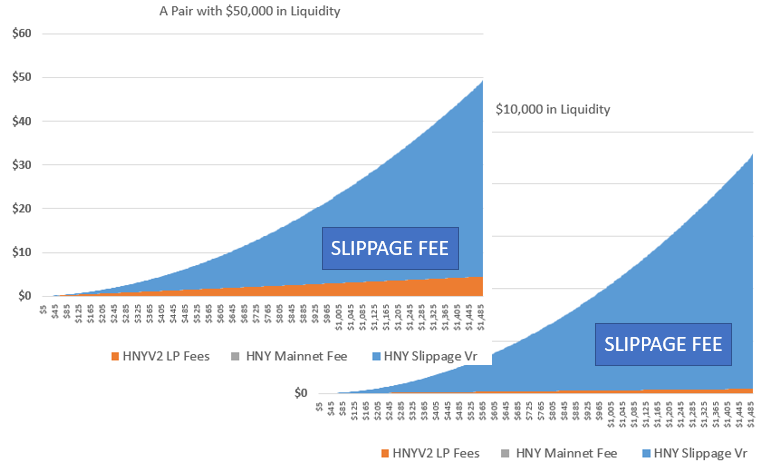

Note: slippage is not linear and UNI slippage fees are favored over HNY slippage fees by 10x

For swaps greater than $1,500 Honeyswap is still getting crushed due to slippage. Less than 1% of our swaps are >$1,500 so the decrease in rate will have little to no affect on profits.

Therefore this is flat 0.25% (which is a 0.05% decrease).

Based on some small sample sizes I believe we can safely assume almost all swaps on Honeyswap are in our target range (less than $1,500). This is largely due to slippage. Given that assumption we can calculate what the revenue for LP & 1hive is and should be.

Last week 1hive received $500 from Honeyswap and liquidity providers received $2,500

Under proposed changes of about 1.3% 1hive and liquidity providers would have shared $13,000 in revenue.

We can decide on what percentage goes to 1hive vs liquidity providers. I am leaning 65% LP / 35% 1hive.

The questions are:

What would happen to LP if they saw their revenue increase 350%?

What would happen to the price of honey if revenue increased 900%?

What would happen to those who use honeyswap saw their fees double?

Would users see their fees double if we saw slippage drop and LP come in?

For me the benefits are enormous and I don’t see myself getting worked up paying an extra $0.20 on a $10 swap or an extra $1 on a $100 swap when we often don’t have the liquidity to even do $100 swap today and we have all seen $15 mainnet fees.

Just remember this is not increasing the fees of making moves on the network or adding liquidity to to pools this is only an increase in fees for doing a swap.

Very well written, thank you. I brought this up back in early November and still think it’s a great move. Liquidity providers are looking for profits, i agree offering better incentives to provide liquidity will bring more liquidity to honeyswap.

Paired with Dosh’s well planned marketing campaign, this could be the boost that “gets a started” again.

Yes, thank you. I linked your article in the post.

One thing brought up several times in replies to your original post was essentially the belief that “we can’t raise fees and remain competitive”

I want to address this very clearly. Yes it is difficult to compete with CEX but is this our audience? We are competing with UNI and therefore we should NOT look at their LP fees but their TOTAL fees which include Mainnet fees. We can raise LP fees to 5% on micro trades and still crush UNI on fees.

We need liquidity and we are still extremely compatible on fees with this proposal.

This is clear and well written, user-friendly I’d say.

I posted a comment also on Discord. I always think from the perspective of the non-expert - someone like me - and I’m wondering if a sort of fee like an exchange would work.

Something like 0.25% if you swap 100$ (random number) / 0.50% if you swap 101-1000$ (again, random number.

Maybe this could make things easier but, no matter what, all it matters is that this “v3” can boost Honeyswap’s liquidity quite much, especially if Eth network won’t be ready to handle the transactions and all the rest.

It makes sense to try this out. I Maybe this idea will help honeyswap and 1hive grow , the only doubt i have is will this encourage less swaps being made on smaller amounts ? Probably yes…

I really like the thinking that has gone into this @Monstrosity, focusing on defining and targeting “micro traders” feels like a good way to take advantage of our competitive advantage relative to Uniswap and other Ethereum decentralized exchanges. To push the thinking a bit further,

From an LP perspective their incentive structure looks something like, fee share + farming incentives / liquidity provided / time. For two pairs that are equal across uniswap and honeyswap, we would expect that in a perfect market those values should be relatively close as LPs move from exchange to exchange looking for the best rate, in practice uniswap will have a big advantage simply because it is a well established brand.

From a trader perspective they care about convenience, security, and overhead cost of their trades. Honeyswap currently has lower transaction fee overhead, the same swap fee percentage, but due to significantly less liquidity much higher slippage. As you point out this give honeyswap a significant advantage for frequent trades of relatively small amounts, as transaction fee overhead scales with the number of trades and not the amount of the trade, and small trades have less impact on slippage.

So here is the rub, if we increase swap fees on trades less than 1500, we reduce the competitive advantage of trading on honeyswap versus uniswap, the closer we get to parity the less reason there is to come over the bridge and trade on honeyswap versus uniswap. I think if there is parity between fees for a given trade, most users would prefer to trade on Ethereum mainnet due to the convenient, composability, and perceived security benefits. If we lose volume as we increase the fee percentage, then we would further reduce fee revenue for both 1hive and LPs, and if we lose fee revenue we would expect more LPs to leave, which could result in more slippage, and further disadvantage for traders. We need to be careful when thinking about changes to the fee structure to think about potential impact on trading volume as a result, and that subsequent impact on actual net revenue for both 1hive and LPs. Counterintuitively, it may make sense to not adjust fees, so that there is a clear and quantifiable advantage for some target segment of traders, and then put our efforts behind documenting and promoting that advantage in order to increase volume, as volume increases profits for LPs would increase, attracting more LPs and reducing slippage, as slippage decreases, the target segment of traders that would be better served by trading on honeyswap increases further increasing volume, in a nice positive feedback loop.

From an implementation perspective, any changes to fees will require some non-trivial engineering work on the contracts, uniswap v2 is not designed in such a way that fees can be set on a per market basis, they are hardcoded globally. DXDao has been working on a fork of uniswap v2 called dxswap that has been updated to allow fee changes via governance on a per-market basis, and we could use that as a base for honeyswap v3, or we could review the smart contracts ourself and make adjustments as needed… but its worth noting that this will take time, effort, and require audits. The currently proposed limit order functionality acts as a layer on top of uniswap/honeyswap v2, so there is no need to to redeploy or change any of the core contracts, I would consider that functionality to be completely separate from the discussion on fees or the promotion of a V3.

I think we should take some time and think about fees further, because I think fee optimization on a per market basis probably makes sense, and optimization around a specific trade size may be a really compelling upgrade for V3. However, I think that the fact that the current fee model presents an advantage for traders of a specific size is actually a really big opportunity for us that we should try and leverage more effectively than we have in the past and would be wary about implementing a fee structure designed to close that gap in order to extract additional revenue at the expense of reducing our competitive differentiation. I think we should use this analysis, and go further with it, to help inform, promote, and attract traders to the platform in order to increase volume. This seems like a great opportunity to give ammunition to the Buzz swarm, help build a better picture of our target users, and create a succinct and compelling value proposition for them to use the platform.

Can we bucket trade size and activity into baskets that correspond to different trading behaviors?

For our initial target trade size, what level of liquidity is necessary?

For our initial target trader demographic, what pairs are they interesting in trading?

3a. How can we reach these traders, should we prompt people who come to the honeyswap website to fill out a survey? Should we consider advertising or promoting the survey on venues like coingecko?

For our initial target trade size, which pairs have the most volume in that range of trade size?

For our initial target trader demographic, what features (e.g. trading view, fiat on/off ramp, ???) do they feel are necessary in order to use the exchange?

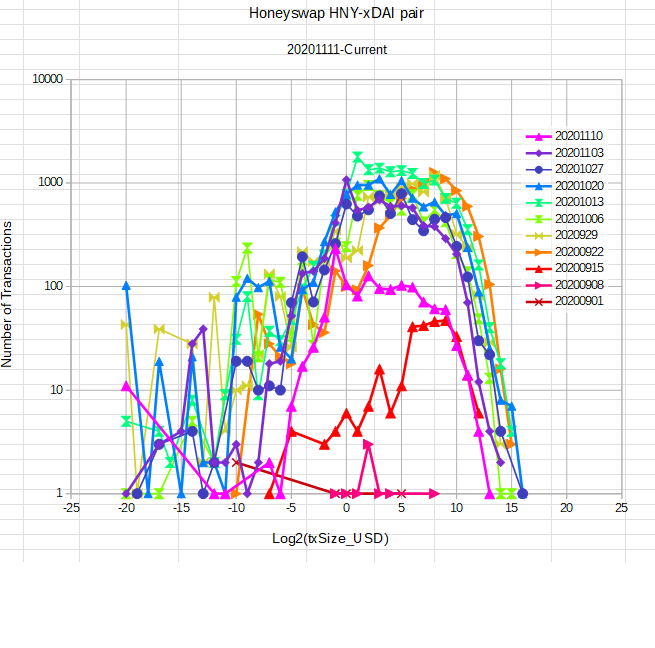

Correction on header 20201111-Current should be 20200901-20201112

So lets see if I have this straight. You want to raise fees to like 1-2% or higher to capture higher profits on these small trades (<$250) and reduce them where we have high slippage and a low number of trades. And this is good? We already are having a hard enough time not just getting people to come to xDAI and use Honeyswap (so much so we don’t have hardly any liquidity) and you want to ‘adjust fees’ to capture more profit to try to encourage larger traders to come here while hammering on the little traders that make up the lions share of the current trading (2^8 and below)

This reminds me of how Coinbase changed fees telling me it would be good for me and would provide higher liquidity so I took my 7 figures of trading away from them. I hardly do anything here in volume like the 7 figures I have done in the past, but sure as shooting if what you propose above goes into effect I won’t be arbing here nor providing liquidity (not as a LP but as a Honeyswap trader normalizing prices to mainnet)

WHO in this forum actually uses Honeyswap to trade or arb to mainnet? I have to pay main net fees to get in and get out with larger quantities of whatever that is traded here, and take on the pricing risk of whatever I move. If the above goes into effect you will basically kill the sub $500 trades and without calculating fees not just for this pair - but all pairs no way to say exactly how much trading this proposal will kill.

I have been steadily trying to work to bring /r/ethtrader in the xDAI/Honeyswap direction. I looked at xDAI and saw low fees and reasonable performance (RPC still a bloody problem issue that needs to be solved once and for all) and so I looked at the microtrading side. Hell low fees is the perfect place for bot trading. Main net in/out is still the price bottleneck for everyone. If there was anything I wanted it was to lower fees say by 1/3 - do this in conjunction with getting HNY on the mainnet with a reverse dutch auction with first 10-20 buyers getting xDAI/1Hive NFTs or who knows what other goodies as a PR event. Offer up to $1K/month in matching LP farming to communities that put LP rewards on Honeyswap and maybe another 1-2K/month (for say 6 months) LP rewards to bring their community infrastructure here.

IF there was one thing I would like to see changed is that the staking contract be set up to pay out two LPs at once (say HNY and DONUT on the HNY-DONUT pair) this way /r/ethtrader IF (big fricken IF here) I can coax carl into getting /r/ethtrader microtipping here (thinking like 10-100 DONUTs which are worth .04 to .4US) we bring /r/ethrtrader eyes, wallets and pockets here. With matching LP funds we can bring part of their financial ecosystems here. My hope was that IF we in /r/ethtrader with carl can bring our DONUT infrastructure here - then perhaps reddit will realize that they can have more than 1 L2 solution to offer subreddits. Getting reddit to formally recognize xDAI as ONE of many L2 solutions (and maybe the first) probably would be the BEST thing short of getting HNY on the main net to help xDAI and 1Hive directly.

These things take time but hell if you pull the cheap trading from under people you will turn away key segments that could be the critical mass to get xDAI and 1Hive into L2 mainstream even if it is on the small end.

Microtraders in Africa and other countries where $1-2/day is a living wage is a real issue - lets try not to toss these people out before they even get a chance to come in.

I’d like to have a control over Honeyswap fees so we could reduce them. I am also interested in bringing curve type stablecoin trading here to take advantage of low fees for stablecoin microtrading arbitrage. I want to lever a low fee network into microtipping models/bots far and wide (beyond reddit). All of this while we see celeste come to fruition and we begin the real work on building on xDAI 1Hive positives while diminishing negatives.

I have been tempted to put up a 5HNY LP proposal for the DONUT-HNY pair as a conditional on /r/ethtrader

(1) bringing DONUT microtipping on xDAI to reddit

(2) adding 50K/week DONUT LP incentives.

Personally I want this to be like 10HNY to pay carl 5HNY for 3 days of work doing getting DONUT microtipping on xDAI as a first step. I have the 10HNY myself If I want to sponsor this beast so I was like this is a wash financially. But from a PR and optics/buzz/business perspective very positive move. So many people wanting to toss out big HNY at ‘big ideas’ and while I am game on some of these things sometimes it pays to start small and work up. Because when you focus on smaller things you create opportunities for the bigger things to happen all on their own.

The risk it what extent will volume be damaged? Will they go back to UNI and pay 500-1000% in fees?

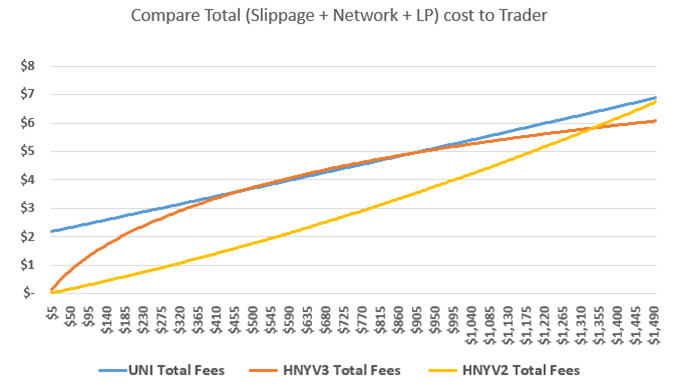

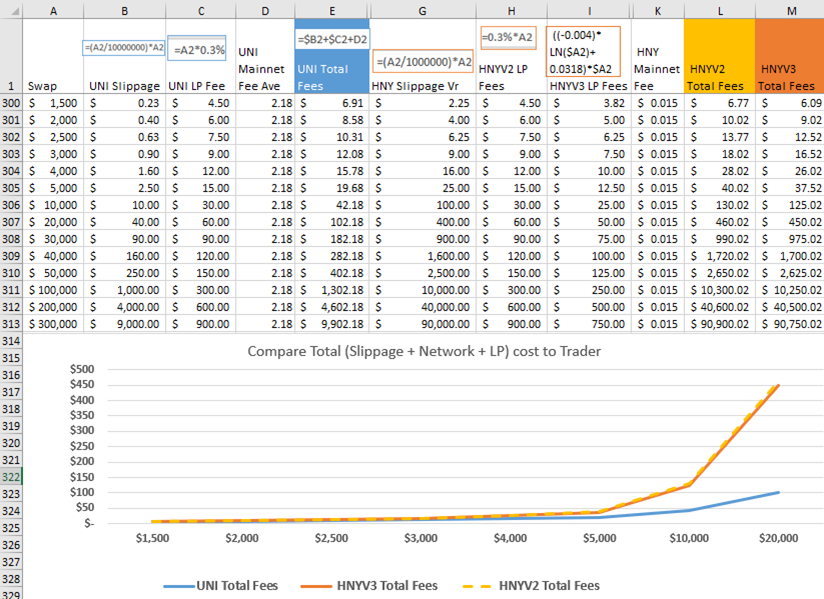

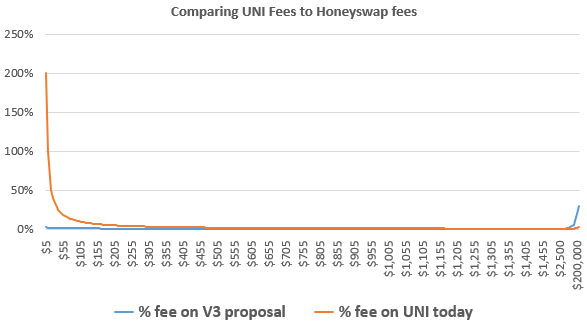

Let us make sure we are grasping the comparison of this fee increase compared to UNI fees.

Right now what it would cost to do a swap on UNI. Not the $2 arbitrary value I used above but the actual… $10.01 for gas fee.

If you compare that to the proposed honey fee increase it would look like this:

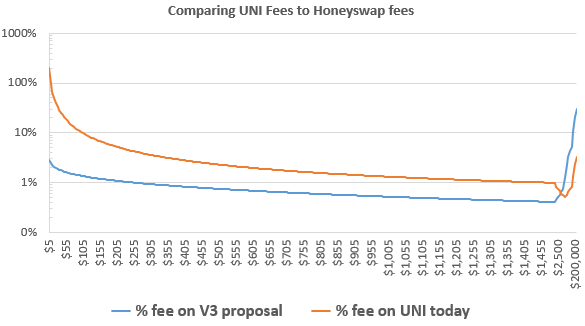

Since you really can’t see that let me put it in log scale for just his one graph.

Let’s filter out some of the noise and just look at the target audience swaps from $20-$100

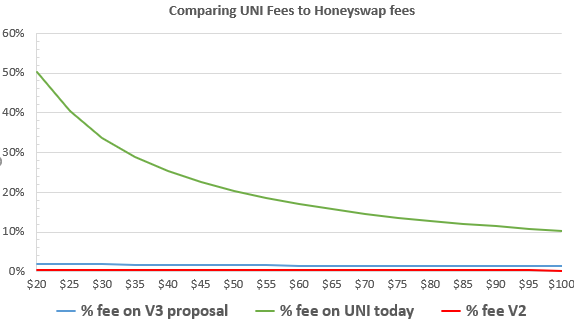

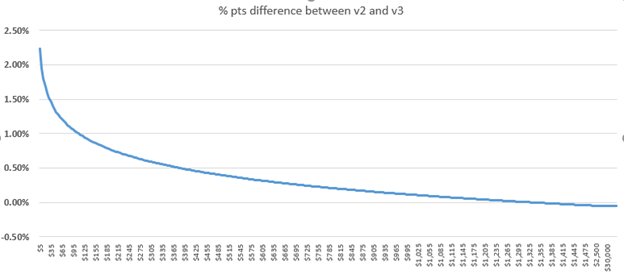

Does this really look like we are eating into our competive edge? It is almost impossible to see the difference between HNY_V2 and HNY_V3 on this graph because UNI fees are so over powering. Let me remove UNI from the graph so you can see what their real difference is…

A little over 2% at the height of the curve is what the fee structure proposes. This is just simply compensating for the slippage and provides a modest increase to the LP.

More great data analysis @Monstrosity, love it. While I’m not an expert by any means, I have done a bit of failing as a trader. Mainly algo trading. Seeing a couple issues with the proposal.

Will this fee structure be intuitive to traders? I know if you do large volume on CEXs, you get a discount. But that is typically done with a large number of trades, and you only get a discount when you’ve got to relatively large sums. Will tiered fees on individual trades and smaller amounts make sense? Would there be an education barrier here?

While there’s a lot of raw data and analysis here, it doesn’t seem like anyone has identified what there ‘micro traders’ are actually doing? I.e.,

I find the small trades very interesting. To add a data point, I do trades in these pleb ranges occasionally. Maybe two or three a week. Mostly just small, casual trades. Maybe half I would have done on other exchanges, maybe half I do just because the fees are so low.

A more intriguing possibility is bots.

Is it possible these are just bots trading price action only on honeyswap? Even if the price is always a bit off from uniswap/other exchanges? Perhaps some bot traders had successful strategies that were priced out of uniswap, so they just ported them over here? If there weren’t too many other bots to compete with, might be a bit easier.

Are there really people that manually trade these small amounts? Genuinely curious.

I wonder, are some of the other micro traders arb bots? It’s been a while since I went down that rabbit hole, and I know it’s complicated, but if the trades are small enough, could you not just keep large (relatively speaking) amounts of each coin on both exchanges? Might not work with uniswap, but could with CEXs with more liquidity and lower fees, if spreads are high enough. E.g. if ETH is more expensive on honeyswap than on Coinbase, buy 0.0001 ETH on Coinbase using your stash of DAI there, immediately sell 0.0001 ETH from your ETH stash here on honeyswap, micro profit? With this strategy, your ratio of coins eventually gets out of whack, and you need to rebalance. But maybe the amounts here are small enough it’s worth it for the occasional rebalancing trip?

Some of the activity just looks strange to me… E.g. the DONUTs/wxDAI pool, where I provide 27% of the $1,408 worth of liquidity , has these swaps for really small amounts.

Is it possible trades are taking strange winding routes through multiple pairs to find the lowest price? Like when I do a trade on uniswap and it shows me it went through like four different pairs?

The vast majority of really small trades are very likely from bots that are arbitraging prices between different pools. For example if you have a DAI/donut pool, DAI/ETH pool, and an ETH/Donut pool there will be small triangular arbitrage opportunities any time any of those prices move significantly. Those strategies can be done without rebalancing between other exchanges, and because honeyswap/uniswap offer flash loan functionality can even be done with minimal capital.

Arbitrage across chain, or across exchange as you suggest is also possible, and its quite likely that a large proportion of our volume is simply from these type of arbitrage traders.

Increasing fees on these micro-trades would likely just result in less volume in these ranges, as the bots would need to wait for greater spreads before trading.

I would love to see dynamic fees which is some function of slippage. For higher slippage pairs this would incentivize liquidity providers to put money into those pairs. As the slippage decreased liquidity providers would have less incentive to put money in those pairs. If the function is reasonable this should result in pairs achieving some optimal slippage such that earnings for LPs and cost for traders is in equilibrium. I suspect the function would be some sort of logarithmic decrease in LP fees with lower slippage.

This should provide a market driven approach that accomplishes the task of pegging fees to expected impermanent loss/ risk to liquidity providers. Liquidity providers get to choose where they put their money so you would expect higher risk pairs (crypto/crypto, or low caps) to have higher fees than low risk pairs (stablecoin pairs or large cap crypto/stablecoin pairs).

Luke has suggested basing dynamic fees on volatility of the pairs directly. However, this requires oracles and more complex logic. I also believe due to the market dynamics of my proposal to base fees on slippage, the result would be similar to pegging fees to volatility and also be more inclusive of all risks to liquidity providers. There may be other factors besides volatility that go into optimal fees, and using a market-based fee structure allows them to be taken into account.

I don’t think this makes sense because the earning for LPs is a function of volume * fees and not just fees. In fact it might be more effective to have the opposite fee structure, such that when slippage is high fees are low (making the total cost to trade lower to accommodate the slippage), then once there is more liquidity and slippage has reduced increase fees.

I’ve been thinking about this more, and while I still think volatility (and historic correlation between the pooled assets) should be an important factor in fee optimization, but I’m also starting to come around the the idea of using governance to adjust fees as it could take into account things that wouldn’t really be possible otherwise, like the competitive landscape and timing of promotional activity.

If LP fees are low when slippage is high there is almost no incentive for LPs to improve the liquidity. If LP fees are low when slippage is low, it doesn’t matter. Any disincentive to LPs results in liquidity being removed, which increases fees, reincentivizing some LPs to join. This creates an equilibrium point. The opposite creates divergence in both directions: pools with a lot of liquidity are incentivized at ever increasing rates to provide liquidity even though the liquidity is pointless, likewise pools with low liquidity are continually disincentivized until there are no funds in them.

I dislike both governance based fees and volatility based fees. I think fees should essentially be decided by market dynamics. The most pure form of this is having LPs state their fees at the time of providing liquidity, then the trader always gets the lowest fees of available bids. However, this is complicated and requires dramatic changes to how uniswap works.

The model I’ve proposed should incentivize liquidity up to the point where it is no longer sufficiently profitable for liquidity providers to add additional funds (not providing liquidity in excess that is unnecessary). It also should have the property of getting liquidity at the lowest required cost, since as fees drop, LPs that require higher fees will leave, and LPs who are willing to accept lower fees will join until you reach equilibrium. I think if we were to run cadcad simulations on this model I am proposing, it would support my hypothesis.

While the incentives here do exist for liquidity providers to some extent under the current uniswap model, there’s no advantage to the traders with increased liquidity besides improvement to slippage. At some point where liquidity is sufficient there is essentially no improvement in total costs for traders.

This ultimately limits the capacity of AMMs to grow and outcompete traditional finance. Under a model where slippage and fees are linked, there is never a point where more liquidity does not improve the experience for traders in a noticeable way. The cost to traders is then only limited by the lowest fees liquidity providers are willing to accept for their capital. This is especially true since on xdai fees are negligible, so there is also no limiting factor due to gas fees.

I think this is the biggest thing we need to focus on (although I think improving fee structures and LP incentives is great).

At the moment, getting onto XDai and trading on Honeyswap is not a particularly intuitive or simple experience. That is not to say it is really hard, but if we can create a better UI for the bridges by making our own then we would vastly improve the experience of the new traders (as far as I can understand there is the xdai bridge and the omnibridge for other erc20 tokens, xmoons are separate again).

I would love to help someone with this but come from an Industrial Design background so my expertise is user centred design and not coding.

I would love to see dynamic fees which is some function of slippage.

@befitsandpiper this is essentially my proposal except I just made slippage static assuming pairs have about $100,000 in liquidity. I would prefer including slippage as well but this adds a little more complexity. I just lean towards action more than designing for perfection.

I don’t think this makes sense because the earning for LPs is a function of volume * fees and not just fees.

@lkngtn but we are not saying we increase Fees on the trader we are suggesting to offset slippage fees by LP fees. so the trader see no difference in the total fees they pay.

I believe next step is to run an experiment. The Luna swarm is looking at this referencing some of the work done here. Thanks to @lkngtn sharing this.

After all this discussion I still think the fee must be dynamic given none of the variables are static. One key flaw in many of the articles I have been reading on this is the omission of the main net fee AND the assumption of infinite liquidity. This is likely because uni’s 100th pair has almost $2M in liquidity meanwhile our number 1, 2, and 3 make up $1M total (with farm rewards).

Their calculations are Fees = LP fees

Why Uniswap studies only talk about lowering LP fees shown in 1 picture. It is the only dominating fee they control.

Meanwhile

Why are we even talking about even considering lowing LP fees when it isn’t even a blip on the fees traders pay? @Eth_Man The arg that target traders are $30 a trade, I will say that is because of slippage. I have been forced out of the market from making larger trades than that.

It would be nice to have equal balance between slippage and LP fees. we are heavily lopsided on slippage fees where as UNI is heavily lopsided on LP fees and mainnet fees.

Speculation without actual data. The data luigy got for me on the HNY-xDAI binned as I have with weekly shows that ‘for the most part’ liquidity didn’t actually increase trade size in fact we got a general decrease of trade sizes. This was indicative of speculators coming into the markets earlier (before LP) biting the slippage bullet to get access to HNY before everyone else (at least in the HNY-xDAI pair).

Accurate and particularly relevant. To date still no real analysis of what Honeyswap traders are doing. I know for a fact that at least one bot appeared doing at first 2xDAI then 1xDAI and later .5xDAI transactions. You can see this as the spikes at -1,0,1 bins in my graphs above for weeks 20201013, 1020, 1027,1103 and 1110.

All relevant points. I can only say from my own experience I weigh two factors. Fees, and then liquidity because I am not a trader typically that needs to execute immediately. My strategy is more of an accumulative model. I also tend to keep liquidity in multiple tokens on multiple exchanges so I can arb trades with liquidity without being depending on passing through main net. This is not capital efficient, BUT if you have a price arb strategy it can be very effective.

I think a complete analysis ‘could’ be done but it would be very time consuming as well as require all of the trading data. Best way to approach this would be a wallet by wallet analysis vs. a trade by trade analysis across all the pairs.

Why is there a target trade size? When we talk about liquidity lets be clear. In bid/ask type exchanges this is people who set down limit orders to provide liquidity against market orders. In $$swap it is by people who place pair liquidity in the exchange to make fees. In both cases ‘volume’ determines the success or failure both of the trader and the exchange or the $$swap liquidity provider. Everything is about the ability for people to trade to build volume.

I have heard both arguments for raising fees to bring in more LP (this only works to a limit because more LP with no change in volume means less return for LP providers), and lowering fees to bring more volume to increase returns to LPs. There is a dynamic balance that needs to be achieved. Personally, while I think uniswap is interesting my trading there is quite limited simply because the fees to cycle (at .6%+2 mainnet tx’s at $5-10 each basically mean a 1.6-2.6% tx fees on a $1K trade (way too high for traders trying to profit off volatility in the 2-4% range - need this to be 10% at least). Even on $5K/trade this is .8-1%. What kills here is the .3% on each side of the trade. My own volume last year as compared with the year before when I had 0 fees on limit orders is down probably 90-95%. When I couple in tax accounting, trade tracking everywhere it just isn’t worth the hassle anymore when I am giving away like 1/2 of my trade profits at 1% of volume vs. maybe .1% (mostly for the market trades I executed) the year before. Worse I have gotten stuck in a trade and ended up underwater because the trade cycling fee put me at a loss when previously I would have claimed profit and exited.

One can just analyze what traders have been doing by doing a wallet by wallet analysis of all the trading data. A simple way to reach some of these people is to offer a reward of some kind for filling out a survey. The survey should be done right where people trade (i.e. Honeyswap) - coingecko afaik is NOT a trading site. Any campaign to get feedback from coingecko users probably won’t be useful.

One just has to look at Honeyswap or Uniswap info to see what people are trading and then do trade analysis.

Use the Honeyswap survey to gather info on (5).

From what I read the median trade size of 16-32 xDAI will be paying higher fees. (so you are going to get lower volume)

I keep hearing this argument but there is a dynamic component to it that is based first on available liquidity now, and fees. It is a catch 22 to believe one can just increase LP and get more volume. What I have seen is that volume drives liquidity. I will give an example. I looked at two LP pairs after bringing DONUTs over and putting it in DONUT-wETH and DONUT-xDAI. I then started looking particulaly at wETH-xDAI because that LP was earning pretty well. In fact that one has generally done pretty well for LPs.

They will just leave xDAI and go look elsewhere. No matter how you look at this the fall back is the main net. Main net tx fees pretty much killing the smaller traders. @Monstrosity what you are ignoring is that people when given a choice against high fee trading and not trading (no matter what the volume/slippage) they will choose to not trade plain and simple. Unless volatility is so high that one can routinely catch 5% price moves even at 2% this is 40% of my profit and I still have to pay taxes on that 60%. As soon as round trip fees approach 1% my volume pretty much drops to zero simply because I am not going to pull trades to earn 1% to pay .2% in taxes to earn a CEX the other 1%. I will do other things to earn that 1% - like seek return that doesn’t require me to pay fees or do much work, as well as reduces risk.

I wanted to argue that we basically lower fees on Honeyswap to something like .2% and see if we can start cranking up volume from those that are trading here because at .2% we only need to increase volume by .25/.15 or 66% to make up the APY for the LPs and fees are down by 33% for traders. FYI at a fixed .05% this would mean a 66% boost straight up in 1Hive revenue. Would I trade 66% more of my volume on certain pairs if the fees were down to .2%. It would probably double my current volume on the xDAI-USDC and maybe the xDAI-USDT pairs.

Would this change make me trade HNY-xDAI or ETH-xDAI more - probably not. What it could do though is make it so that once we hit a certain liquidity level that traders would come to use xDAI/Honeyswap vs. using the main net for trades. We still have to pay to get on and off xDAI (2 main net txs) but once here we just need that .1% against the potential slippage to make up for those 2 main net tx’s. As volume increases and returns for LP providers increase. Liquidity will increase.

As a ETH-SAI trader for a time I put liquidity into the Uniswap contract because I ended up catching part of the fees I paid doing the trades (this was the surest way to reduce my fees - being a LP) - even though over time so much volume moved into that contract that I ended up exiting it.

Personally what I want is a exchange that gives me back the 0 fee limit and .25% market orders and ideally allows me leverage. The idea of something like DYDX on xDAI with more tokens supported to me seems more appealing than anything else at this point. Trying to cross these trades into the main net is fraught with a lot of hazards (liquidity, pricing). Thinking of something like dex.io and 1inch where one tries to use multiple markets to find the best prices for a trade. Barring a full out fork/port of DYDX I see lowering Honeyswap fees and maybe taking part of the increased 1Hive returns and putting them out for LP stake farming. Pay out to the LP providers with some of the .05% profits in both the pair tokens as a redeposit into the staking contract like Badger does with 50% of the sett returns.

I saw the analysis, I think it would be good to look at a pair that doesn’t have artificially low trade sizes. cred stimulates smaller transaction sizes. Better to look at a eth-xdai or btc-xdai.

Where will they go?

You are right it is a catch 22. No benefit to add liquidity and I can’t trade because no liquidity. I just don’t get why someone would put $1000 into a pool for $0.1 a day at the risk of IL.

Maybe I am too focused on what I would do… If LP fees were 0% it would have no impact on my trades. Occasionally when I try to do a $500 swap I make 10 swaps of $50 ea over the course of a week. to avoid the 10% slippage fees but still end up paying 1-2% in fees so I don’t blink an eye over 0.3% it isn’t a priority relative to the elephant in the room (slippage).

All my real trading unfortunately still has to be on mainnet and it isn’t Honeyswap LP fees running me off.

started” again.

started” again.

, has these swaps for really small amounts.

, has these swaps for really small amounts.