At the moment, there seems to be a variety of incentives which lead to different inflation preferences.

Very short term: pump price immediately. Proposals such as capping supply or burning HNY.

Short to mid term: Funding farms to erase impermanent loss or increase HNY price by improving Honeyswap. Or simply more interested in Honeyswap than other 1Hive projects.

Long term: Wants high price eventually, but sees the value in distributing more HNY to create all sorts of new proposals in and outside Honeyswap, Celeste, etc.

These are all reasonable preferences depending on one’s circumstances.

Maker has an interesting dynamic inflation policy where making good decisions for the DAO’s main goal, keeping DAI stable and popular, burns MKR. Instability mints MKR. This aligns short term and long term interests. I don’t know how this would be applied specifically to HNY, but perhaps the inflation system should be thought of in terms of aligning incentives.

If HNY is minted or burned in response to certain outcomes then consensus on improving those outcomes is pretty easy to reach. This could have a very positive effect on the community as more HNY holders will share the same goals.

Good Idea / Deflationary rewards could feet and help this initiative.

I believe an 3% to 4% yearly inflation could be acceptable and help the project to recover some interest.

Price action is short term, but establishing the value of the community is long-term and is our best shot of retaining what we currently have.

Why does price continue downward? Because people are selling! Literally! Sell pressure is real and directly related to current outflow of HNY minus the demand. #People milking the honey pot Economically, that’s par for the course with public goods; the curse of the ‘free rider’. Look at Gresham’s law, “… circulating currency consisting of both “good” and “bad” money quickly becomes dominated by the “bad” money. This is because people spending money will hand over the “bad” coins rather than the “good” ones, keeping the “good” ones for themselves.” Applying this to the crypto space, people are going to dump the crap coins every chance they get and hang on to the harder assets.

There’s a lot of competition in the crypto space and as optimistic and idealistic as many are, HNY is not going to hold value under many of these overly inflated models that are not supported by the demand necessary to satisfy these models. We must harden HNY before we can even think that it will be a stable means of funding development. HARD HNY = $$$ for Development… point blank.

Lastly, this is not mutually exclusive from many of the other proposals out there regarding inflation. It would just require the rates at which we inflate to be toned down.

Gersham’s law does apply. LITERALLY speaking, HNY is exchangeable, transferrable, divisible, and lives in the wallets of many amongst other coins that have the same potential to be exchanged and sold. Modern economic theory aside, people get rid of the shizz coins first and hodl the good ones… Gersham’s Law!

This entire thread is inherently monetary. Issuance=Monetary

I don’t think you’re using the terms money, public good, or free rider properly. You can issue lots of things besides money, such as stocks. My point is HNY isn’t being weighed against other crypto for its utility as a medium of exchange. It’s an asset. If you wanted HNY to become a currency you’d want a relatively stable price which would undermine all the other goals of holders.

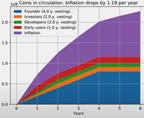

There’s been some discussion in the luna discord channel today which hammers out some further details on a potential dynamic issuance model that a number of 1hive members, including myself, believe is a good long term policy.

The idea is centered around our conviction voting model and targeting a fixed percent of total supply in the common pool to fund proposals. If the supply in the common pool exceeds the target percent of total supply (due to inflows from project revenue entering the common pool), the common pool switches into a burn paradigm. While the common pool is less than the target, we switch into an issuance paradigm.

The simplest version of this policy is a simple flip between a specific issuance rate and a specific burn burn, however a continuous policy is likely preferred instead. An example of a pretty simple continuous dynamic policy would be to have the issuance rate equal to the following equation:

1 - (common pool supply / target supply).

If the issuance rate is negative, the common pool would be in a burn paradigm, while if the issuance rate is positive the common pool would inflate, diluting HNY holders over time. The incentives here end up being similar to the incentives Maker has around issuance, although instead of the rate being made through discretionary governance, it follows a simple formula.

One downside of this formula or ones like it is the issuance is no longer capped. While incentives are aligned for HNY holders to reduce outflows to frivolous project, and so switch into a low issuance or burn paradigm, there is no simple story around issuance and passive shareholders may have less confidence in the long term inflation rate.

It is possible to set a maximum issuance with a policy like this. But the choice of maximum issuance is necessarily an arbitrary decision, and it’s unclear what it should be set to. If the maximum issuance is set too low, we risk choking the DAO by artificially preventing outflows to valuable projects that the community wants to fund.

Personally, I am against setting a maximum issuance policy. I believe the incentives of dynamic issuance are strong enough that the community would tend to reduce issuance over time anyway, and support only proposals that are believed to bring positive value. However, if we were to set a maximum issuance policy, setting once close to this current inflation rate of 32% seems like a good starting point.

I know @lkngtn and @Eth_Man also have opinions on this topic, but this is my view from the discussions we had today.

This is a great idea. If you are concerned about the cap being too low, one compromise can be to have decreasing issuance for a number of months until reaching the final cap (so 60% 50% 40%… 10%), but I think the sooner the policy is “set in stone” the better.

There is a vote to reduce issuance from 60% to 30%: https://1hive.org/#/vote/6 (Note the UI is a bit buggy, the buttons keep flashing on and off, we’re aware of this).

If you vote in favour of it, your HNY will be locked until the vote either passes and is executed or until the end of the voting period. This is likely to mean voters don’t vote until near the end of the vote.

Public Good: “A public good is a good that is both non-excludable and non-rivalrous. This means that individuals cannot be effectively excluded from its use, and use by one individual does not reduce its availability to others.” So the most common example of a public good is national defense. Individuals within a nation cannot be excluded from this. The public good is not HNY, but instead, the ecosystem. Regardless of whether one wants to participate, we cannot exclude someone from the ecosystem and more specifically, from the faucet. Honestly does not matter whether we’d categorize the ecosystem as a public good… the point the was being made was that individuals–for, against, or indifferent to the cause–have access to the ecosystem and faucet, regardless of their contributions… Do you agree?

This leads to the next point regarding the free rider problem:

Free rider problem: “The burden on a shared resource that is created by its use or overuse by people who aren’t paying their fair share for it or aren’t paying anything at all.” – The shared resource is the ecosystem and faucet. Let’s take the faucet. Regardless of your contribution to the faucet, if you register, then you receive the same amount as any one else. The free rider problem applied to this would state that there will be individuals who exploit the faucet, sell their HNY and not contribute to the ecosystem because it is there. Do you agree that there are likely individuals who receive HNY without any intention to contribute to the ecosystem?

This leads to my next point regarding money:

Money: “The characteristics of money are durability, portability, divisibility, uniformity, limited supply, acceptability.” Money should also be a store-of-value.

Do not confuse money with currency, which is not a store of value. HNY holds all those characteristics. You could buy other cryptocurrency with HNY. Regardless of our mission with HNY, it has these properties and in turn, is a form of money. Regardless of whether you agree with that, hopefully you agree with the notion that it has value. The very notion of value creates hierarchies. ‘Good’ versus ‘Bad’ money, or crypto, or project, or what ever you want to call it is valid for this situation entirely. No one has unlimited resources, which implies that people are deciding what they will keep versus sell, and buy versus not buy. Do you agree that people (EVERYONE) wants something that will retain value?

Bitcoin=Money=Asset

Stocks are arguably money and money (not currency) is arguably an asset… Take Bitcoin… Hardest money known to man; hardest asset known to man. Calling something money does not mean that it will facilitate transactions; instead, it could facilitate transactions. I could buy things with shares of TSLA if I really wanted to. I wouldn’t, given what it would take, but I could trade partial shares with an agreeing party… This is all irrelevant. Given HNY properties, its ability to facilitate transactions will not diminish.

The same functions of dynamic issuance can be ascertained under a max supply cap. The only difference is that value is distributed with respect to proportion of remaining common pool as opposed to the quantity of the pool. Moreover, indefinite inflation and maximum supply are not mutually exclusive. Many assets in this world have a maximum supply, but indefinite inflation. Take gold for instance, which inflates year to year at a decreasing rate… We need increasing supply at a decreasing rate such that the total supply tends towards a value. I agree with:

Lastly, let’s consider the risk-return. Worst case scenario with too low a max supply, we back a new crypto with the value of HNY to meet our needs. Worst case scenario without a max supply, our holdings are worth nothing and majority of participants in this ecosystem leave. Who’s taking these losses well?

The idea of creating HNY as a hard asset and having a secondary asset which is inflationary is certainly interesting… it would require a lot of changes in how we think about the HNY token and its role within our community, but this is definitely a possible option to consider.

In particular I found interesting how a Balancer pool is able to be controlled by a smart contract with a specific policy that could issue tokens or buy them back under certain market conditions.

I will be honest, due to volume of post on this thread I haven’t been able to keep up to date with all the ideas and therefor I am assuming that many of these topics have been repeated. However, rather than capture in another post I think this would be the best place for the data I collected.

This is a look at several other token/coin projects and their issuance & issuance policy and what impact it had on their price, assumptions are made.

Preface:

All the poor performers lacked clarity of any kind or their token supply (CRO) was insanely high. Is the data I have sufficient to make the claim that these are the reasons, no. But based on looking at all of these projects I believe it to be a reasonable assumption. The only main outlier in my opinion is BAND, I can’t explain its performance at the time of writing this.

Conclusion:

In regards to an issuance policy; Inflationary/deflationary, a slower issuance over a long time, a fast issuance over a short time, cap or no fixed cap. None of these seem to matter to price in the grand scheme of things. Traders(those who drive price up) just want to know a plan that is fairly reasonable. What is fairly reasonable? I suspect something less than what CRO did where they have 100B total supply and are sitting on 80% in a common pool essentially (but it still has a expected market cap of $8B at current price). Two other quick examples

Sushi token was falling in price until they made an announcement they would cap their token, just an announcement. There is no actual cap and the token is up 3x

CRV has one of the highest issuance of 3B tokens over 6years and the price has found a bottom around $0.35 in oct and is now 2x, this means it has a theoretical market evaluation >$1B.

Summary of project issuances:

Obviously a lot more work was put into this, more so than what you just see here but maybe this will bring some value to others.

I haven’t yet performed any analysis on these coins/tokens but I did collect some data and grouped the projects into 1 of three categories:

Those with a max supply (BNB, SNX, SUSHI, CRO. KuCoin)

Those without a max supply but they have an issuance policy (CRV, UNI, KNC,PICKLE)

Those without a max supply and no issuance policy (BAND, HT)

It is apparent to me that the following are the biggest contributing factors to coin/token price.

• project itself – I did not go into great detail here

• having a token supply policy

It did not appear to me that the issuance rate or max supply really had much of an impact at all:

Because crypto is fast moving I focused on this past year, cycles and market movement. No statistics was performed on the follow just my opinion based on analyzing them closely. Also, note some may seem odd at first but considering we just went through an alt crash so every coin is suppressed if they saw growth in last two weeks they weren’t poor performer necessarily.

Strong Performers – won’t elaborate on these two:

• BNB – consistent

• SNX – Doing very well

BNB SNX

Honorable Mention – these both have a longer history so that commonality put them in their own category and arguably no different than the questionable performers:

• KNC – Longer life than the others seeing 4x over last year but coming down from a top following market last 2 weeks

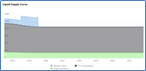

• BAND - Longer life than the others seeing strong growth over last year but coming down from a top following market last 2 weeks (outlier, performing relatively well give no cap and 2 ICOs and 1 IEO)

KNC BAND

Questionable Performance:

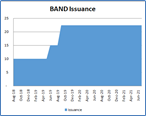

• UNI – Volatile price but recently in last two weeks following market price

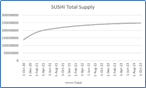

• SUSHI - very high release price but since recently following of market in the last 2 weeks.

• PICKLE – surprisingly one of the most cyclical yet stable tokens showing a flat ROI until the hack

• CRV – insanely high release price but since it has been flat with a possible following of market in the last 2 months.

UNI Pickle SUSHI CRV

Poor Performers:

• KuCoin – This is the only one I didn’t yet provide an issuance curve because their documentation doesn’t align with reality. And maybe their changes to their plan have something to do with their price.

• CRO – it has a max supply but its current circulating supply is only 20% of their token supply which we don’t know for sure what or when or how it will be released.

• HT – It appears they have a project issue going on. I really didn’t even want to include them after looking into them. CRO

Really interesting discussion, really enjoyed reading through all the ideas here.

In the meantime, the proposal to cut the issuance rate to 30% has passed https://1hive.org/#/vote/6 !

I personally consider that a step forward. Also, it might be a good idea to edit the first post with this new rate to avoid confusion for people who are not yet up-to-date.

An issue I see with the dynamic issuance model is the risk of a death spiral. Suppose the dynamic model goes into effect and we are unable to generate much revenue, as is the case right now. You could end up with high inflation and that high inflation will discourage adoption and the creation of new projects thus preventing revenue generation and the cycle repeats.

Correct me if I’m wrong, but MKR, which pulled off the dynamic issuance policy, had its product out there almost from the start of issuance and demand for DAI/SAI was solid. 1Hive may not be able to function with a dynamic model until the HNY starts flowing into the common pool thanks to a profitable project.

We can cap the issuance rate with a throttle. But yes, there is risk of overinflation and failure of the project. This is a risk that essentially all new organizations have. But HNY holders ultimately make the decisions around issuance indirectly through passing spending proposals. HNY holders have incentives not to overinflate.

In comparison to a fixed issuance schedule, dynamic issuance produces lower inflation in all cases except the one where spending exceeds the original fixed issuance rate. By setting a max issuance in combination with the dynamic policy we cover this case as well and force overspending to be followed by relative austerity, and increased difficulty of proposals passing.

We could still reduce this maximum issuance rate as we grow and reach new steady states, although I would be cautious about lowering this max rate on a fixed schedule or prematurely, since reducing issuance is not really reversible once we make that decision.

The max issuance rate is currently 30% so this risk exists. Revenues are so low at the moment that almost all spending will be replaced by inflation rather than revenue inflows. So yes, you could stop inflation by stopping spending, but then nothing gets passed. No new projects, no new revenue, death spiral. This model doesn’t work well when there is little revenue.

I think RogueTwo might be on to something by saying the issuance policy shouldn’t be set in stone. What issuance policy works now?

We might be able to go as low as 10% max issuance for the dynamic policy. I think going lower than that risks us starving the DAO though, and I still prefer a higher max issuance to give us flexibility. We currently have a real inflation of about 30%, so this is a 1/3 budget cut at current prices. But, cutting issuance may also raise prices which will reduce our issuance needs. Hard to predict exactly what happens here.

Since we are already well above the target ratio for the common pool (likely 10-20%, whereas the current ratio is about 28%) a 10% max issuance policy wouldn’t constrict supply much for another 6-8 months at least (we will still be burning HNY from the common pool over this period). It’s possible our inflows will increase a lot and/or our outflows will decrease over this time period so 10% or less will be all the issuance we need to fund proposals by then.

BNB

BNB  SNX

SNX KNC

KNC  BAND

BAND UNI

UNI  Pickle

Pickle  SUSHI

SUSHI  CRV

CRV CRO

CRO